7 Tax Planning Strategies for Startups & Small Business

By Mike Smith, Iowa Center Small Business Tax Preparer at the Iowa Center for Economic Success

As a Small business owner you understand the ebb and flow of your business better than anyone else. It may be the holiday rush or spring fever – no matter when it is, it is a good time to focus on tax-planning and savings. Let us take a quick look at seven strategies you can employ to make the most of your tax planning efforts.

Strategy 1: Review and update your financial records.

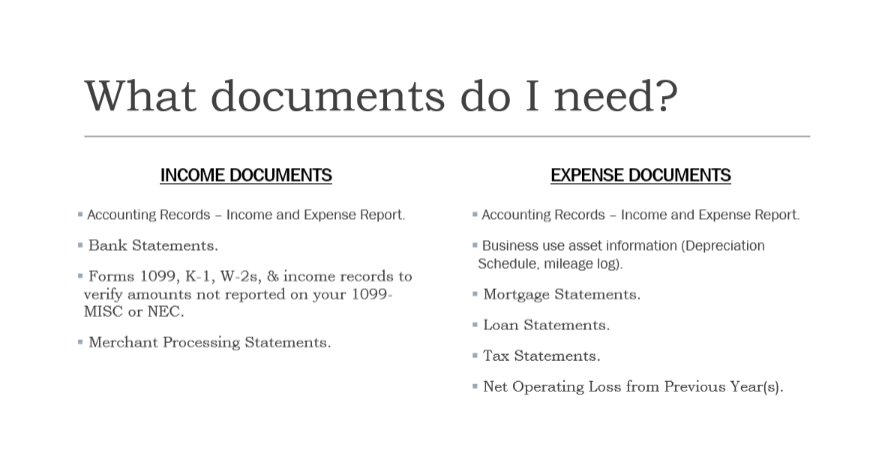

Accurate and up-to-date financial records are essential to good tax planning. Take this time to review and update your financial records; identify sources of income; the cost of goods sold; and other expenses. Organize your receipts, invoices, expense reports and other financial documents.

If you do not currently have one, consider purchasing a reliable accounting software platform.

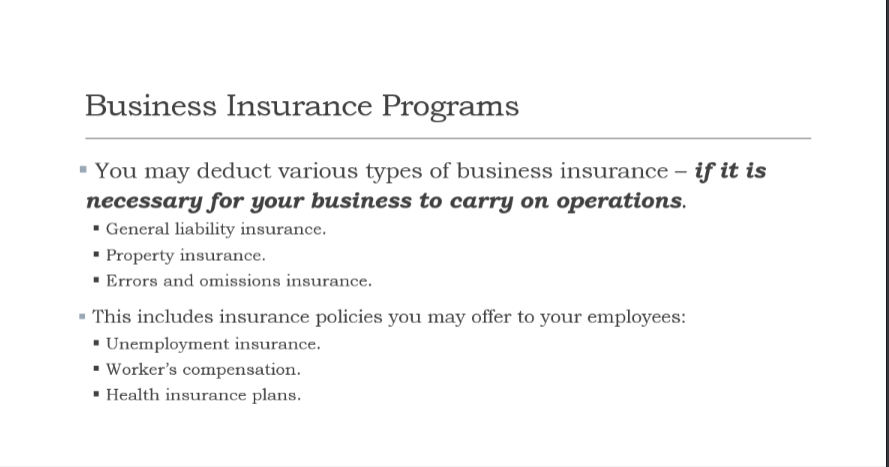

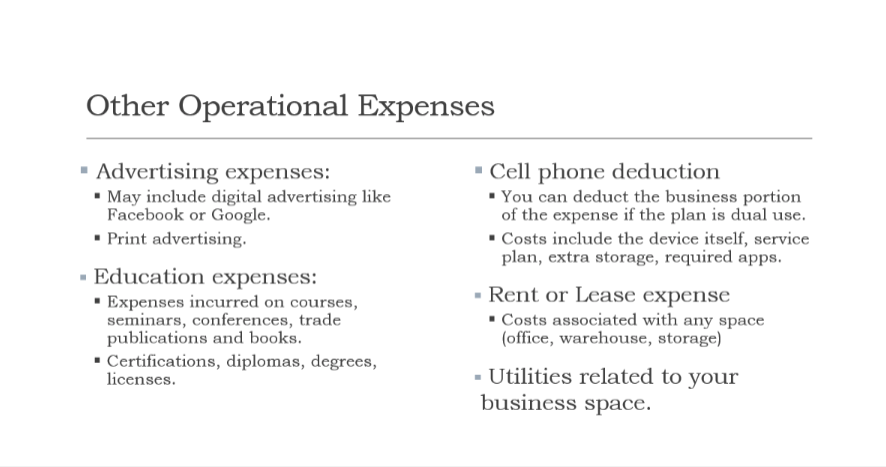

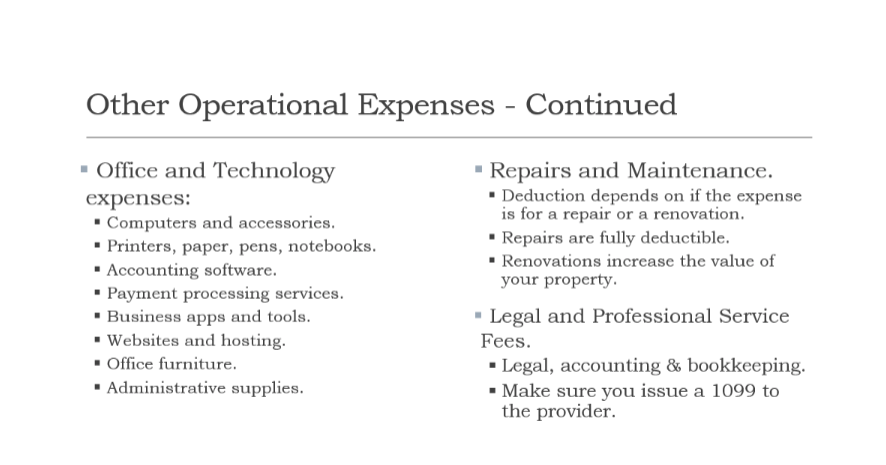

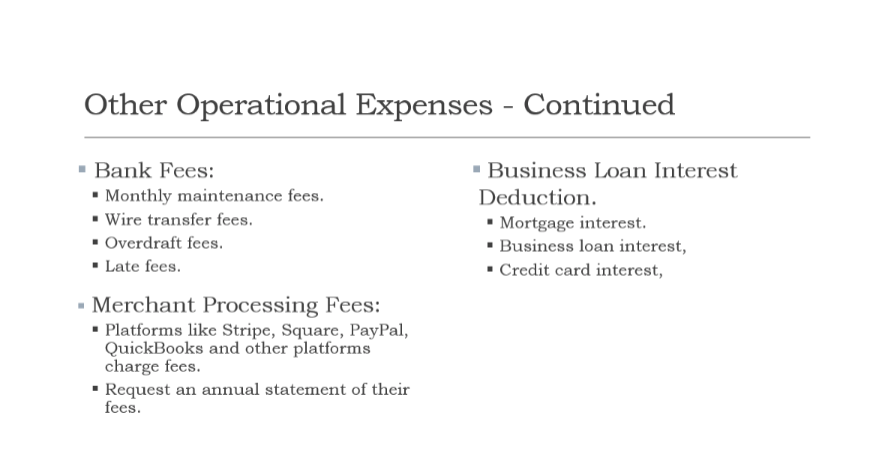

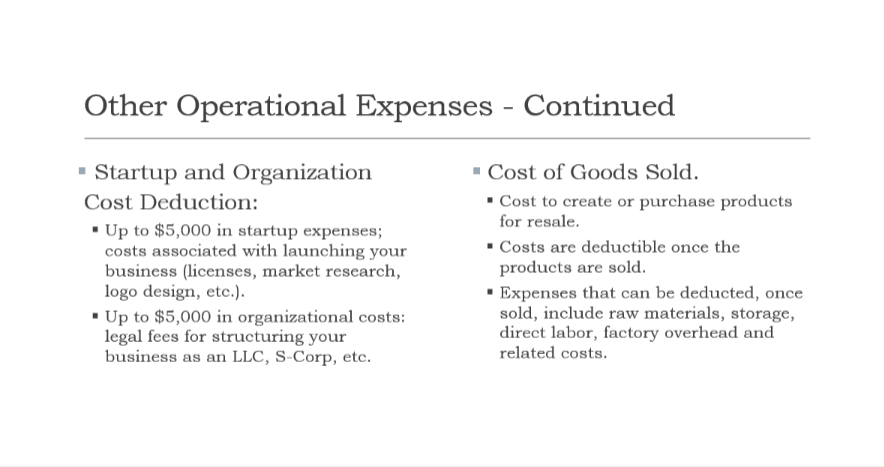

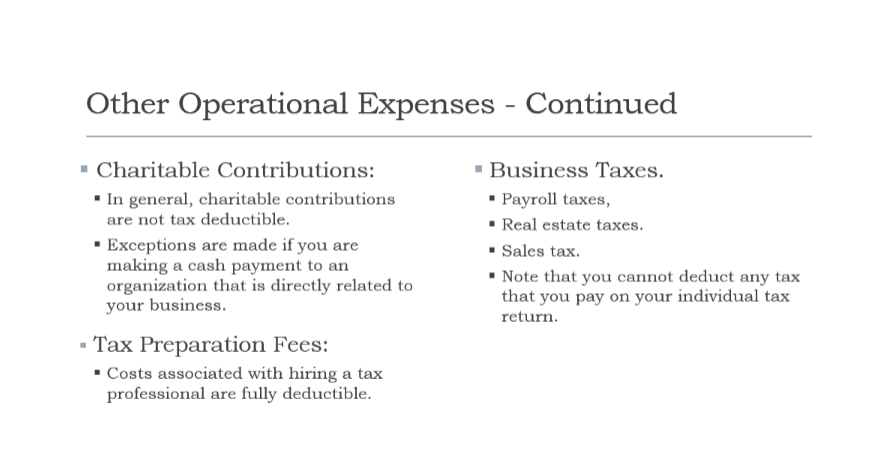

Strategy 2: Evaluate business expenses.

One of the easiest ways to save money on taxes is to review your expenses and identify areas where you can reduce costs. Analyze all your expenses to see if any of them can be categorized as deductible business expenses.

Consider looking at:

Reducing your travel budget.

Canceling unused subscriptions.

Renegotiating contracts.

Defer payments where possible.

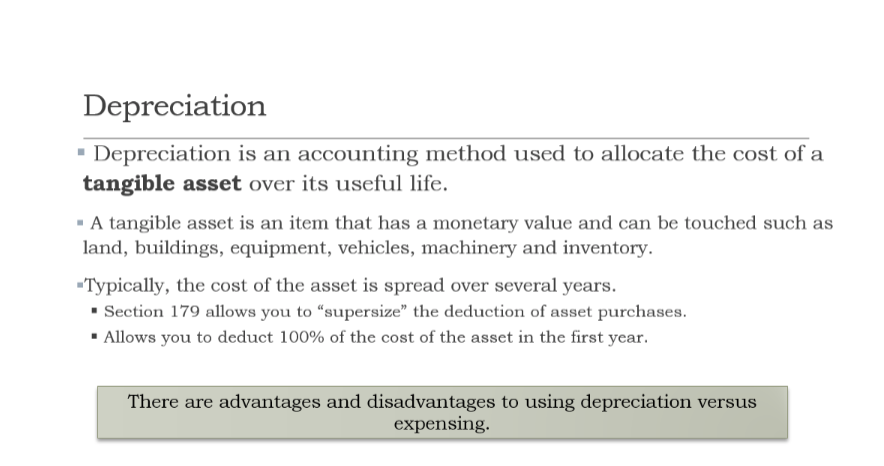

Strategy 3: Assess depreciation and capital costs.

This is a great time to review your capital assets and assess what depreciation you have claimed. If you are not claiming depreciation, review your capital equipment on hand (usually a unit cost of $3,000 or more) and develop a depreciation schedule.

Strategy 4: Take advantage of all deductions and credits you are eligible for.

There are a number of deductions and credits your small business may be eligible for. Take this time to research them and see if you might be able to take advantage of any of them. Check out the IRS website Credits and deductions for businesses. Internal Revenue Service for ideas and information.

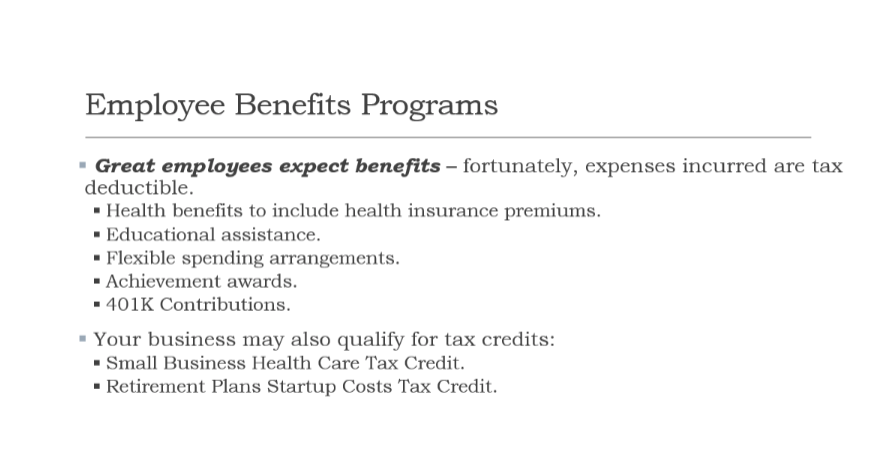

Strategy 5: Plan for retirement contributions.

Contributing to a retirement plan for you, as well as your employees, not only secures your financial future, and theirs, but also offers potential tax benefits as well as helps with employee retention.

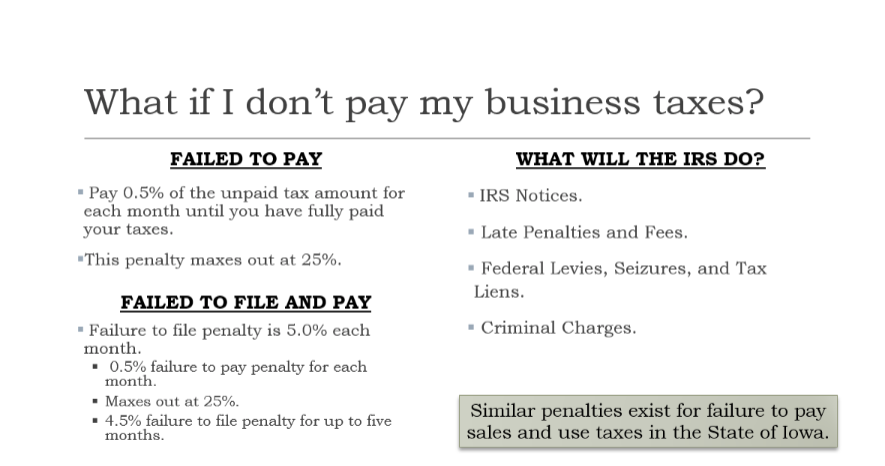

Strategy 6: Estimate your tax liability.

Based upon your business evaluation estimate your tax liability for the coming year. Develop a proactive plan to pay your income and employment taxes to avoid a large tax bill at the end of the year as well as potential penalty and interest payments.

Strategy 7: Consult a small business tax professional.

A tax professional can assist you in staying up to date with the complex and ever-changing tax laws.

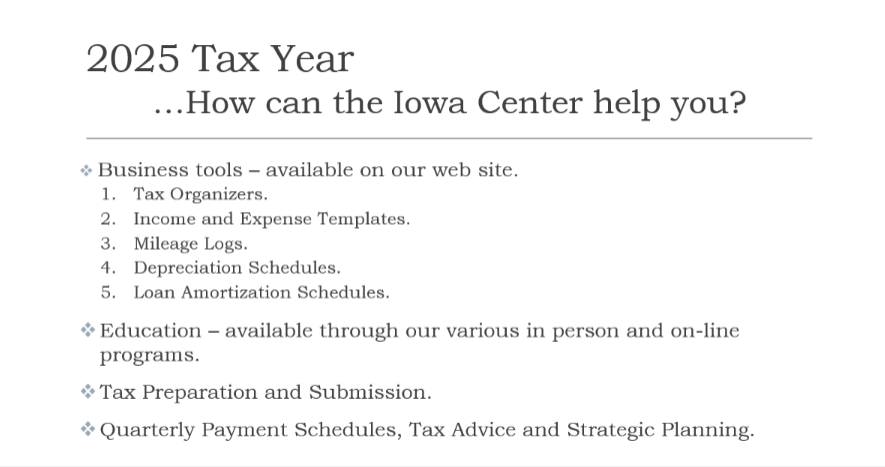

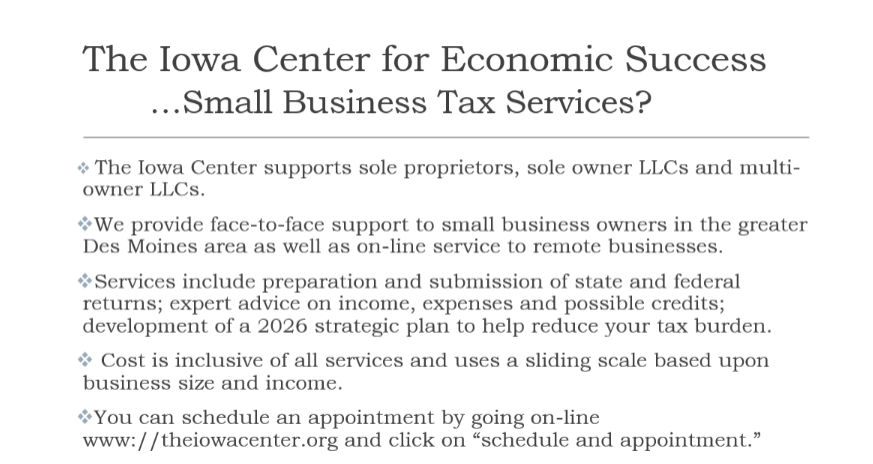

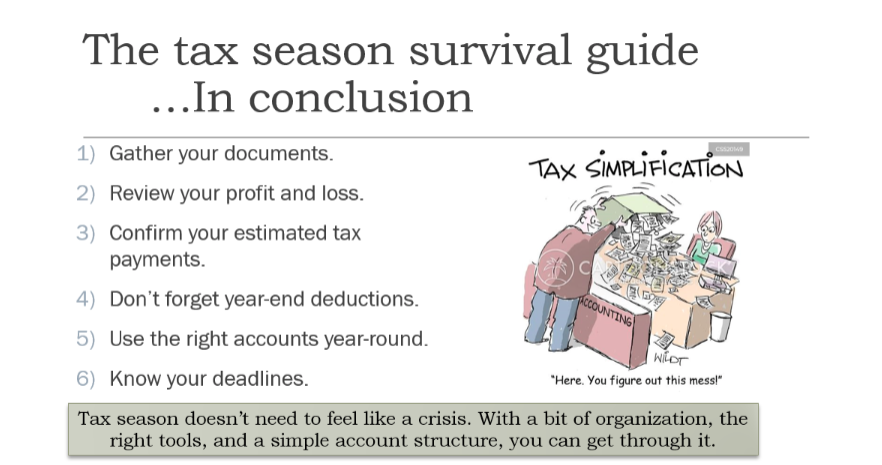

Are you a small business owner, startup founder or indivudual that could use some help with your tax planning and filing? The Iowa Center can help! Learn more about their Tax Services and schedule an appointment to make sure you are headed in the right direction with your taxes! In the meantime, view the presentation below to get educated on the small business tax process.